Understanding Opportunity Cost

Picture this:

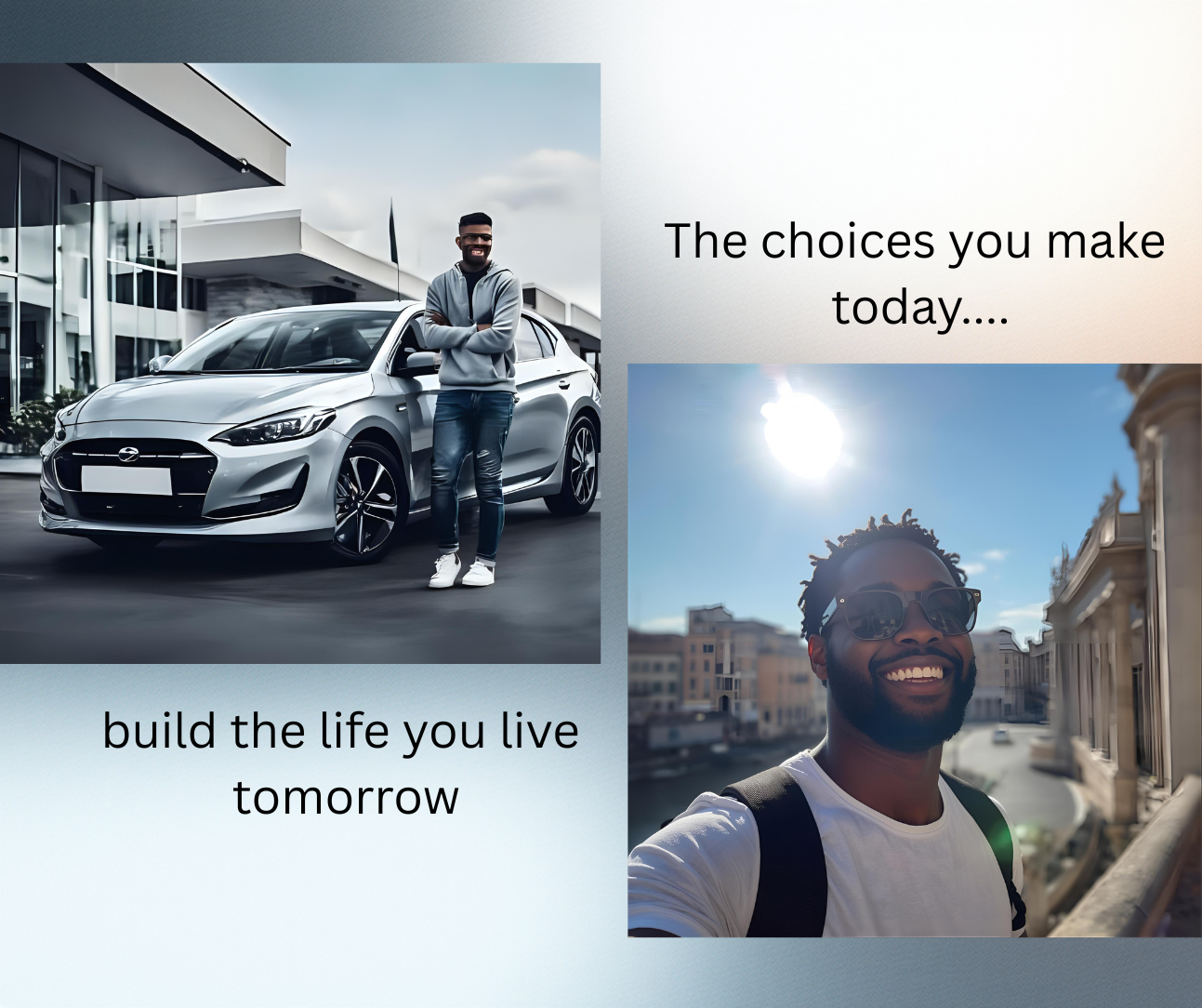

You’ve just landed your first full-time job. Your paycheck hits the account, and for the first time, you feel that sense of independence — you earned this. You’ve been driving the same car since high school, and it’s showing its age. A shiny new model catches your eye. The dealer says, “It’s only $600 a month.” You do the math — it seems doable. After all, you deserve something nice after all that hard work.

But before signing the loan papers, pause for a moment.

What if that same $600 a month could quietly build a different kind of freedom?

Meet Alex

Alex is 23, fresh out of college, and just starting out in a marketing role. Like most young adults, Alex wants to enjoy life — travel, go out with friends, and upgrade that old car. But after seeing a few posts about investing early, Alex decides to take a closer look at what that $600 monthly payment really costs over time.

If Alex invested $600 a month instead, earning an average 8% annual return, after 10 years that money could grow to roughly $108,000.

That’s not just money — that’s choice.

It could be a down payment on a dream home, the capital to launch a business, or the foundation of early retirement. Meanwhile, the new car — worth $35,000 today — would likely be worth less than $10,000 by the time it’s paid off.

The Real Cost You Don’t See

This is what economists call opportunity cost — the hidden price of the choice you didn’t make. Every dollar you spend today is a dollar that can’t be working for you tomorrow.

But opportunity cost isn’t about guilt — it’s about awareness. It’s about realizing that your dollars carry potential energy. Where you direct that energy determines the kind of life you’ll build.

The Ripple Effect of Choices

Alex decided to compromise. Instead of buying the new car, Alex bought a reliable used one and started investing the difference. That one choice — made in their twenties — changed the trajectory of Alex’s financial future.

Years later, those early investments opened doors that many peers couldn’t afford to walk through: the freedom to leave a job that didn’t align with their values, taking time off for travel, starting a side business, and buying a home with less stress.

All because Alex saw the hidden cost behind a shiny short-term upgrade. That’s the power of seeing the invisible cost of your choices. Every “yes” today means a “no” somewhere else — but when you make that choice consciously, you stay in control of your financial story.

Try This Reflection

Before making your next big financial decision, ask yourself three questions:

- What am I gaining right now? (Comfort? Convenience? Status?)

- What am I giving up later? (Growth? Flexibility? Security?)

- Is this trade-off aligned with my future goals?

Sometimes the experience is worth it — but when it’s not, those dollars can become your partners in building long-term stability and choice.

Small Choices, Big Future

Understanding opportunity cost is about living intentionally — not perfectly.

You’re not being asked to skip every joy in the moment, only to make sure every dollar has a job that serves your future self as well as your present one.

Because whether you notice it or not, opportunity cost is always working in the background.

The only question is — will it work for you or against you?

Follow Growing Gift for more tips and tricks to make smart financial choices and build a strong, empowered future.